Life insurance in California provides financial security, covering debts, funeral costs, and living expenses, ensuring your family’s well-being in high-cost areas.

This article will explain what life insurance is, the different types available, why it’s necessary, and how to choose the right policy in California.

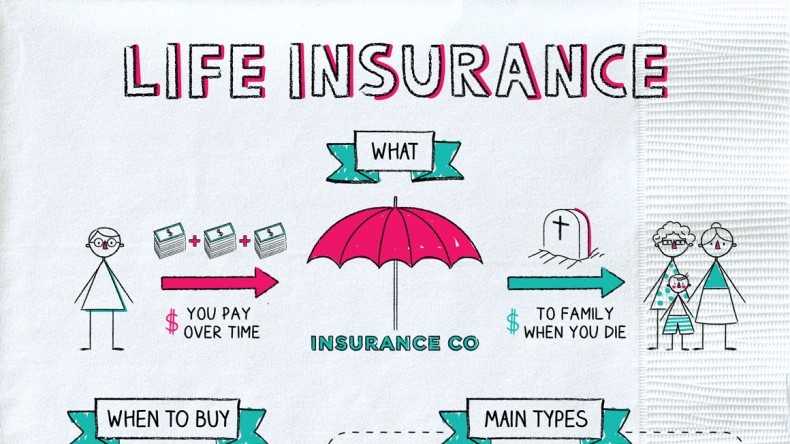

What is Life Insurance?

Life insurance is a contract between an individual and an insurance company. In exchange for regular premium payments, the insurer provides a lump-sum payout to the designated beneficiaries upon the insured person’s death. This payout helps cover various expenses, such as funeral costs, debts, and living expenses for family members who depend on the insured for financial support. Life insurance ensures financial security for loved ones after the policyholder’s passing, offering peace of mind during difficult times.

Why Is Life Insurance Important in California?

California is one of the most expensive states to live in, with high housing, healthcare, and living costs. Life insurance helps provide financial security for your family and loved ones in case something happens to you. It ensures that they can maintain their lifestyle, pay for ongoing expenses, and avoid financial burdens during a challenging time. Having life insurance is a responsible and caring choice for anyone who has dependents or financial responsibilities.

Protect Your Family’s Future:

If you’re the primary earner, life insurance ensures your family can continue to pay for essential needs if you unexpectedly pass away. It replaces lost income, so your loved ones can keep up with rent or mortgage payments, food, and children’s education. Life insurance helps protect your family’s financial future, ensuring they don’t have to worry about finances during a difficult time. It provides security for those who rely on your income for daily expenses.

Cover Debts and Final Expenses:

Life insurance helps cover any outstanding debts or funeral costs, so your family won’t be burdened. Without it, your loved ones may have to take on the responsibility of paying off these expenses themselves, creating financial stress. Funeral and burial costs can be expensive, and life insurance ensures your family has the money to handle them. It’s a financial safety net, giving your family the time to grieve without worrying about money.

Also read: Tom Selleck Health – A Comprehensive Look At His Wellness Journey!

California’s High Cost of Living:

California’s high cost of living makes life insurance even more important. Cities like Los Angeles and San Francisco have expensive housing, healthcare, and education costs. Life insurance provides a way for your family to maintain their lifestyle if you’re no longer there to provide financially. It helps ensure they can pay bills, stay in their home, and cover daily living costs without your income, offering peace of mind in one of the most costly states.

Types of Life Insurance in California:

There are several different types of life insurance, each designed to meet the needs of individuals and families in various situations. Below are the most common types of life insurance policies:

Term Life Insurance:

Term life insurance is one of the simplest and most affordable types of life insurance. It provides coverage for a specific period, such as 10, 20, or 30 years. If the insured person passes away within this term, their beneficiaries receive the death benefit. However, if the policy expires and the insured person is still alive, no benefits are paid, and the policy ends.

Advantages of Term Life Insurance:

- Lower premiums compared to permanent life insurance

- Simple and straightforward coverage

- Ideal for covering temporary needs, such as paying off a mortgage or funding a child’s education

Disadvantages of Term Life Insurance:

- Coverage ends after the term period expires

- No cash value or investment component

Whole Life Insurance:

Whole life insurance provides lifelong coverage, meaning it remains in place as long as you continue paying your premiums. In addition to the death benefit, whole life policies also build cash value over time, which can be accessed through loans or withdrawals.

Advantages of Whole Life Insurance:

- Lifetime coverage

- Cash value accumulation

- Fixed premiums for the duration of the policy

Disadvantages of Whole Life Insurance:

- Higher premiums than term life insurance

- Can be more complicated than term life policies

Universal Life Insurance:

Universal life insurance is a type of permanent life insurance that offers flexibility in both premiums and death benefits. It allows policyholders to adjust their coverage and premium payments, as well as accumulate cash value over time. However, the cash value and premiums can fluctuate depending on the performance of the insurer’s investments.

Advantages of Universal Life Insurance:

- Flexible premiums and death benefits

- Cash value accumulation

- Potential to adjust coverage based on changing needs

Disadvantages of Universal Life Insurance:

- Premiums can increase over time

- Investment performance may affect cash value

Final Expense Insurance:

Final expense insurance is a type of life insurance designed to cover funeral and burial costs. It is typically a smaller policy, often chosen by individuals who want to ensure their funeral expenses are taken care of without burdening their loved ones.

Advantages of Final Expense Insurance:

- Covers funeral and burial expenses

- Easier to qualify for than other types of insurance

- Affordable for many people

Disadvantages of Final Expense Insurance:

- Smaller death benefit compared to other types of life insurance

- Limited to covering only final expenses

How to Choose the Right Life Insurance Policy in California:

Choosing the right life insurance policy depends on several factors, such as your age, health, lifestyle, financial goals, and the needs of your family. Here are some tips to help you make the best choice:

- Assess Your Needs: Evaluate your financial responsibilities, including debts, family income needs, and education costs. This helps determine the coverage amount and policy type suitable for you.

- Determine the Type of Life Insurance: Choose between term life insurance (affordable, temporary coverage) and permanent life insurance (lifetime coverage, cash value). Select based on your long-term and affordability needs.

- Compare Life Insurance QuotesObtain quotes from multiple providers to compare prices. This helps ensure you get the best coverage at the most competitive rate for your specific situation.

- Consider Your Budget: Ensure the policy’s premiums fit your budget. Choose affordable coverage to avoid financial strain while maintaining enough protection for your family’s needs.

Also read: Ma Health Connector – An Easy Guide To Health Coverage In Massachusetts!

Check the Insurance Company’s Reputation:

Research the company’s reputation, customer service, and claim reliability. Look for solid financial ratings and positive reviews to ensure your beneficiaries are properly supported.

How much does a $1,000,000 life insurance policy cost per month?

The cost of a $1,000,000 life insurance policy can vary widely based on several factors, including:

- Age: Younger individuals generally pay lower premiums.

- Health: Healthier individuals typically receive lower rates.

- Type of Insurance: Term life insurance is usually less expensive than whole life insurance.

- Gender: Women tend to pay lower premiums than men due to longer life expectancy.

- Lifestyle: Smokers or those with high-risk lifestyles may pay more.

On average, a healthy 30-year-old could expect to pay around $50–$100 per month for a term life policy. For whole life insurance, the premium could be significantly higher, potentially $400–$1,000+ per month.

For a precise quote, it’s recommended to request a quote from an insurance provider.

FAQ’S

1. What is the difference between term life and whole life insurance?

Term life insurance covers you for a specific period, while whole life insurance provides lifelong coverage and builds cash value.

2. How much life insurance coverage do I need?

The amount of coverage depends on your financial responsibilities, such as debts, income needs, and family requirements. A common recommendation is 10-15 times your annual income.

3. Can I change my life insurance policy in California?

Yes, most policies allow changes such as adjusting coverage or adding beneficiaries, but it’s important to check the policy terms.

4. What is final expense insurance?

Final expense insurance is a smaller policy designed to cover funeral and burial expenses, providing a financial safety net for your family.

5. Is life insurance expensive in California?

Life insurance premiums vary, but due to California’s high cost of living, they can be higher than in other states. Comparing quotes can help find affordable options.

Conclusion

Life insurance is essential for ensuring your family’s financial security, especially in high-cost areas like California. It helps cover debts, funeral costs, and ongoing living expenses, offering peace of mind during difficult times. By understanding the different types of life insurance, you can choose the right policy that fits your family’s needs and budget, providing long-term stability.